The Deal to End Surprise Medical Bills Finally Gets Approved

Scope Of The Protections

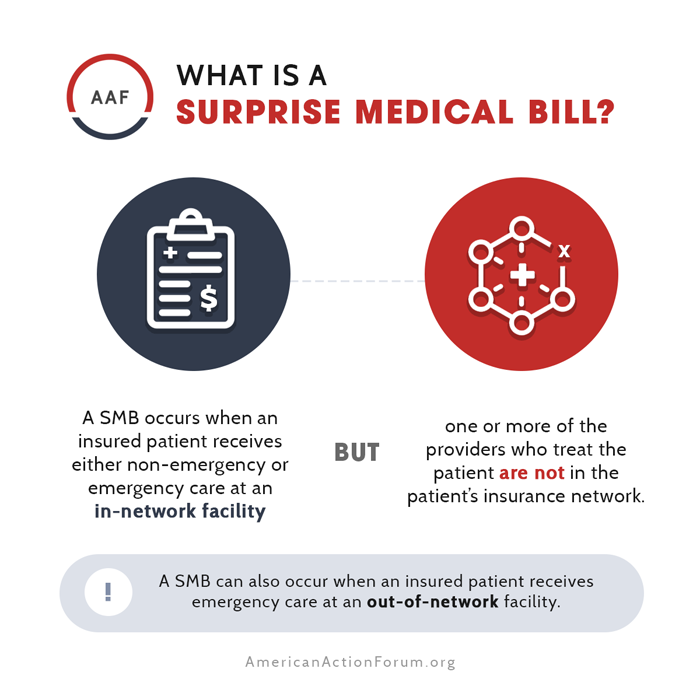

Consumers would be protected from surprise medical bills when they receive care in both emergency and nonemergency settings; the protections would extend to out-of-network air ambulances. As a result, patients would be protected from surprise bills in situations where they have little or no control over who provides their care.

Emergency Services (Including Air Ambulances)

Patients would be protected from surprise medical bills for emergency services from the point of evaluation and treatment until they were stabilized and could consent to being transferred to an in-network facility. Protections would apply whether the emergency services were received at an out-of-network facility (including any facility fees) or provided by an out-of-network emergency physician or other provider.

As mentioned, the bill would also extend to air ambulances, which have a history of sending sky-high surprise medical bills to patients with critical medical situations. To increase transparency regarding air ambulances, air ambulance providers and insurers would have to submit two years of cost and claims data to federal officials for publication in a comprehensive report. In addition, the legislation establishes an advisory committee on air ambulance quality and patient safety.

The bill would not extend to ground ambulances. This is likely because few states, to date, have regulated in this area, which is complicated by the fact that many ground ambulance services are provided by local government entities. The legislation, however, does call for a special advisory committee to recommend ways to best protect consumers from these surprise medical bills and improve transparency for ground ambulance services (including through the disclosure of charges and fees and improved consumer education and disclosures).

Nonemergency Services

Patients would be protected from surprise medical bills for nonemergency services provided at an in-network facility but by an out-of-network provider. Today, a patient might receive a surprise bill from a nonemergency out-of-network provider that provides, say, ancillary services (such as those delivered by a radiologist, anesthesiologist, or pathologist) or specialty services needed to respond to unexpected complications (such as those delivered by a neonatologist or cardiologist).

Here, the bill allows for some voluntary exceptions to surprise medical bill protections but only if a patient knowingly and voluntarily agrees to use an out-of-network provider. For instance, if a patient wants to select an out-of-network orthopedist for a knee replacement or an out-of-network obstetrician for a scheduled delivery, the patient could waive the federal protections (and thus could be charged a balance bill). Because the patient is knowingly choosing to see an out-of-network provider, the reasoning goes, the additional cost is no longer a “surprise” to the patient.

The bill would also allow certain providers to request that a patient sign a consent waiver. But this exception is relatively narrow and generally more protective of consumers than state laws that allow for consent waivers. This exception would only be allowed in nonemergency situations. And providers could not request a consent waiver if 1) there is no in-network provider available in the facility; 2) the care is for unforeseen or urgent services; or 3) the provider is an ancillary provider that a patient typically does not select (e.g., a radiologist, anesthesiologist, pathologist, neonatologist, etc.). The bill identifies a list of providers that could not ask for a consent waiver, and federal officials would be able to identify additional providers in future rulemaking.

For providers who are eligible to ask a patient for a consent waiver, the provider must generally notify the consumer in writing 72 hours before services are scheduled to be delivered. This notification must include a good-faith cost estimate and identify available in-network options for obtaining the service.

Settling Payment Disputes

While all stakeholders agree that patients should be taken out of the middle of disputes between insurers and providers, much focus has been on how to then settle payment disputes between insurers and out-of-network providers. In general, insurers and employers have favored adoption of a benchmark payment standard (meaning an insurer would pay, say, its median in-network rate to an out-of-network provider), while providers have favored arbitration. As noted above, the No Surprises Act does not include a benchmark payment standard but rather relies on voluntary negotiations between insurers and providers, backed up by arbitration if negotiations fail.

Arbitration Process

The legislation would establish timeframes for the arbitration process and impose other guardrails. For instance, insurers and providers would have 30 days to engage in private, voluntary negotiations to try to resolve the payment dispute. If negotiations fail, either party may, within two days, request independent dispute resolution. Presumably if there is no settlement and no request for arbitration, the provider would accept the amount paid by the insurer.

The arbitration process would be administered by independent dispute resolution entities subject to conflict-of-interest standards. The federal government would establish the independent dispute resolution process, including a list of entities available to take cases.

The bill adopts “baseball-style” arbitration rules: each party would offer a payment amount, and the arbitrator would select one amount or the other with no ability to split the difference. The decision would then be binding on the parties, although the parties could continue to negotiate or settle. Multiple cases could be batched together in a single arbitration proceeding to encourage efficiency, but those batched cases would have to involve the same provider or facility, the same insurer, treatment of the same or similar medical condition, and would have to occur within a single 30-day period.

There are two rules that could help deter overuse of the dispute resolution process. First, the losing party would be responsible for paying the administrative costs of arbitration. If a case is settled after arbitration has begun, the costs would be split equally unless the parties agree otherwise. This rule increases the financial stakes for pursuing long-shot cases. Second, the party that initiates the arbitration process would be “locked out” from taking the same party to arbitration for the same item or service for 90 days following a decision. The goal of this provision is to encourage settlement of similar claims. Any claims that occur during the lock-out period, however, could go to arbitration after the period ends.

Arbitration Factors

Arbitrators would have flexibility to consider a range of factors. This includes any relevant factors raised by the parties, but not the provider’s usual and customary charge or the billed charge. By explicitly prohibiting arbitrators from considering provider charges, the bill attempts to help limit any potential inflationary effects if arbitration leads to settlements well above the amounts insurers typically pay to in-network providers.

Optional factors that an arbitrator could consider include, among others, the level of training or experience of the provider or facility; quality and outcomes measurements of the provider or facility; market share held by the out-of-network health care provider or facility, or by the plan or issuer in the geographic region in which the item or service was provided; patient acuity and complexity of services provided; teaching status, case mix, and scope of services of the facility; any good faith effort—or lack thereof—to join the insurer’s network; and any prior contracted rates over the previous four years. Arbitrators would also be able to consider the median in-network rate paid by the insurer. Federal officials, in implementing the dispute resolution process, might opt to provide more guidance on the use of these factors in the future.

The same general factors would apply to air ambulance providers, with some adjustments such as the location where the patient was picked up and the population density of that location, and the air ambulance vehicle type and medical capabilities.

Interaction With State Laws

To date, 17 states have enacted comprehensive surprise billing laws, and another 15 states have more limited protections. The No Surprises Act would defer to existing state laws with respect to state-established payment amounts. Thus, if a state law already sets a payment amount for a surprise medical bill dispute (as many of the states with comprehensive protections have done), this payment mechanism would continue to govern disputes between insurers and out-of-network providers in that state for the fully insured plans they are able to regulate. Said another way, state payment standards would not be preempted or otherwise displaced by the No Surprises Act.

States would be free to pass surprise billing laws in future years as well, whether with a payment standard or arbitration that uses different criteria. Federal officials might be able to offer future guidance on the extent to which state standards can be used in place of the federal arbitration process.

Enforcement

With respect to insurers and employers, the bill would adopt the same enforcement framework as the ACA and HIPAA: states would continue to be the primary regulators of fully insured health insurance products (with back-up enforcement by the federal government if a state fails to substantially enforce the law). The Department of Labor would continue to regulate self-funded plans.

With respect to providers, the bill would allow states to require a provider (including air ambulances) to comply with the new standards. If a state fails to substantially enforce those requirements, the federal government would step in to do so. This federal backup enforcement would allow the federal government to impose civil monetary penalties against providers of up to $10,000 per violation. Federal officials would also have to establish a process to receive consumer complaints on surprise medical bills.

Other Provisions

The No Surprises Act includes many more provisions that are critical to protecting patients from surprise medical bills. For instance, providers would be required to provide uninsured consumers with a good faith estimate of costs before a health care service is delivered. If the eventual charges for the service were “substantially” higher than the good faith estimate, the patient could invoke the independent dispute resolution process to challenge that higher amount (although the patient might have to pay a fee to do so).

Federal officials would have to regularly report to Congress on the impact of the No Surprises Act. The Department of Health and Human Services, for instance, would have to report on the legislation’s impact on factors such as provider consolidation, health costs, and access in rural areas. The Government Accountability Office would have to issue three reports on issues such as the legislation’s impact on network adequacy and provider payment rates, as well as the independent dispute resolution process (including whether providers that use this the process have relationships with private equity firms).

Finally, the bill would provide funding to states to set up all-payer claims databases, make changes to current external review and continuity of care provisions, and require the Department of Health and Human Services to finalize rules related to provider discrimination (with the goal of preventing discrimination against providers acting within the scope or their license or certification).

Most importantly, the bill would remove the patient from the dispute process. Patients in emergency situations are especially vulnerable to the opaque and confusing nature of the health care system. The bill would prohibit surprise bills for all out-of-network emergency services, including air ambulance, and patients will pay in-network cost-sharing for these services. In addition, the bill would create safeguards such that providers and plans must give advanced notice of potential charges and network status.

- The “No Surprises Act” protects patients from surprise medical bills. The proposal provides that patients will only be responsible for their in-network cost-sharing amounts, including deductibles, when receiving medical care.

- The proposal takes important steps to moderate the impact of non-marketplace, government-set rates by using the median in-network payment rate only as one consideration within the arbitration process.

- The inclusion of an Independent Dispute Resolution (IDR) process will allow physicians to challenge unfair payments from health insurance companies. Importantly, this proposal improves physician access to the IDR process with the exclusion of a monetary threshold and the inclusion of “batching.” Further, the arbitration criterion takes important steps forward by ensuring that the process is fair and reflects the marketplace, by including consideration of previous contracting history among the factors the arbiter may consider.

- The start of the IDR process is appropriately aligned with the implementation of the prohibition on surprise bills. This alignment will ensure that physicians have access to a mechanism to address inappropriate insurer payments that is concurrent with the prohibition on surprise bills.

COVID Spending Package with

0 Comments