If you’re in Illinois and looking for affordable health coverage, here’s what you need to know:

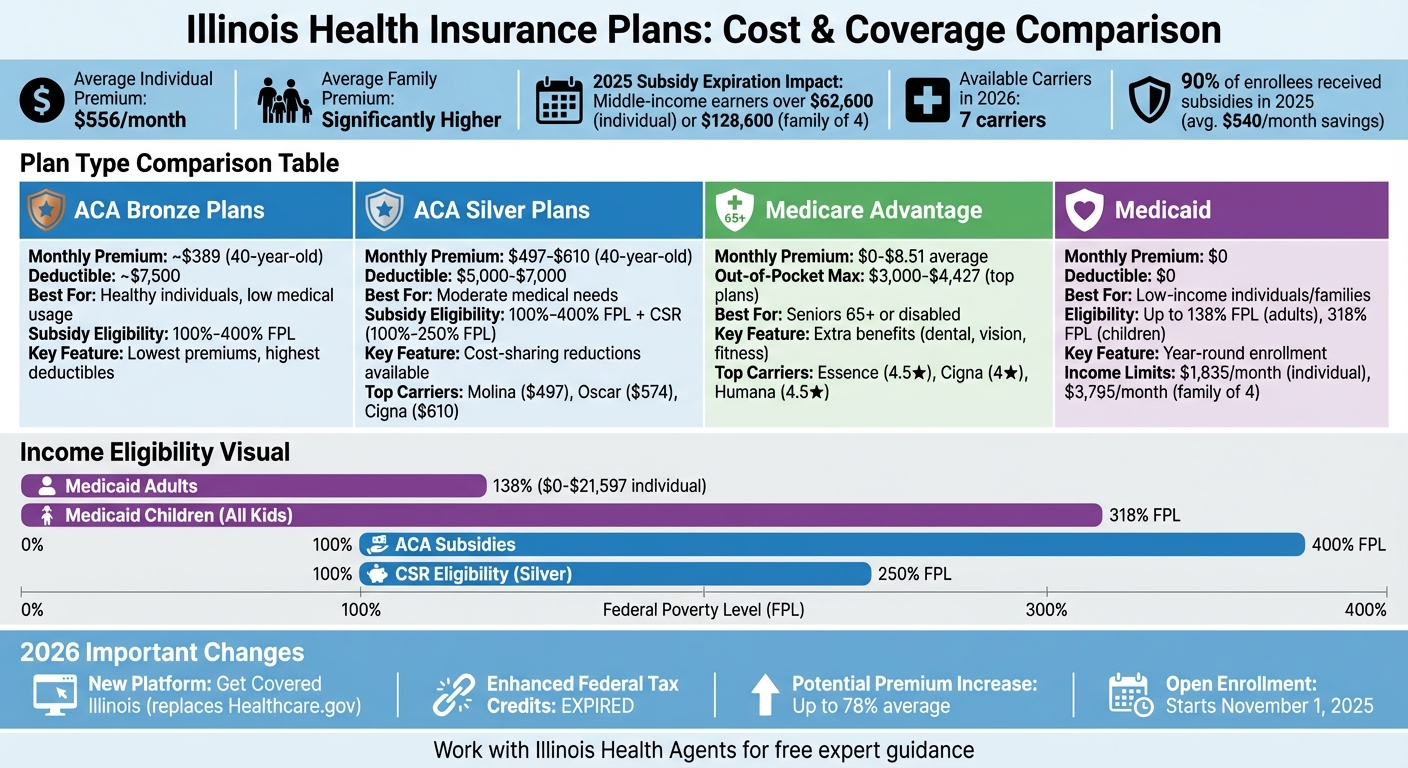

- Average Costs: Individual health insurance averages $556/month. Family plans are significantly higher.

- Subsidy Changes: Federal subsidies expired in 2025, leaving middle-income earners without financial help. This impacts individuals earning over $62,600 and families of four earning above $128,600.

- Marketplace Update: Illinois launched its own platform, Get Covered Illinois, replacing Healthcare.gov. Only 7 carriers remain for 2026, limiting options.

- Plan Options:

- ACA Plans: Subsidies available for incomes 100%-400% of the Federal Poverty Level (FPL). Bronze plans have low premiums but high deductibles (~$7,000). Silver plans may offer cost-sharing reductions for lower out-of-pocket costs.

- Employer Insurance: Often cheaper if your employer covers a large portion of premiums.

- Medicare Advantage: Options for seniors, with some $0 premium plans and extra benefits like dental or vision.

- Medicaid: Free or low-cost coverage for low-income individuals and families. Enrollment is open year-round.

Key Takeaway: Balancing premiums, deductibles, and out-of-pocket costs is critical. Use Illinois’s new marketplace or consult a licensed broker to find the best plan for your needs.

Illinois Health Insurance Plans Comparison: Costs, Coverage, and Eligibility Guide

Understand Your Health Insurance Options With Get Covered Illinois

sbb-itb-a729c26

Types of Budget-Friendly Health Insurance in Illinois

Illinois residents have several affordable health insurance options to consider: ACA Marketplace plans, employer-sponsored insurance, Medicare, and Medicaid. Knowing your eligibility can make it easier to find the right coverage without breaking the bank.

ACA Marketplace Plans

Starting November 1, 2025, Illinois introduced its own state-run platform, Get Covered Illinois, replacing the federal HealthCare.gov system. This platform is the go-to for income-based subsidies, like Advance Premium Tax Credits (APTC), which help reduce monthly premiums. In 2025, nearly 90% of Marketplace enrollees in Illinois received subsidies, saving an average of $540 per month. This brought premiums down to about $190, with 24% of participants paying less than $10 monthly.

Eligibility for these subsidies usually applies to individuals earning between 100% and 400% of the Federal Poverty Level (FPL). Additionally, those earning up to 250% of the FPL can take advantage of Cost-Sharing Reductions on Silver plans, which lower out-of-pocket costs. Marketplace plans offer a balance of affordability and comprehensive coverage, but it’s worth comparing them to employer-sponsored plans to see which provides the best value for your situation.

Employer-Sponsored Insurance

Health insurance offered through your employer is often a budget-friendly option because employers typically cover a large portion of the premium. These plans also tend to provide access to broader provider networks. However, if the portion of the premium you’re responsible for feels steep compared to your income, you might still qualify for subsidies through the Marketplace. Illinois residents can use the Employer Health Plan Affordability Calculator to decide whether switching to a Marketplace plan makes more financial sense.

If employer-sponsored insurance isn’t an option, Medicare or Medicaid may be the next best alternatives, depending on your age or income level.

Medicare and Medicaid

Medicare is designed for Illinois residents aged 65 and older, as well as younger individuals with qualifying disabilities. Many seniors opt for Medicare Advantage plans, which often feature $0 premiums and extra perks like dental and vision care. To help navigate the variety of Medicare options, the Illinois Senior Health Insurance Program (SHIP) offers free guidance.

Medicaid, on the other hand, provides low-cost or even $0 premium coverage for eligible low-income residents. In Illinois, Medicaid covers adults aged 19–64 with incomes up to 138% of the Federal Poverty Level (around $21,597 for an individual). For children, the "All Kids" program extends Medicaid coverage to households earning up to 318% of the FPL. Unlike Marketplace plans, Medicaid enrollment is open year-round. To make the application process easier, Illinois residents can check a box on their state tax returns to share their information with Medicaid and Get Covered Illinois.

Top ACA Plans for Budget-Conscious Buyers

In Illinois, residents have access to seven insurance carriers offering Marketplace plans through the Get Covered Illinois platform. These include Blue Cross Blue Shield of Illinois (BCBSIL), Ambetter, Cigna, MercyCare HMO, Molina Healthcare, Oscar Health, and UnitedHealthcare. If you’re looking for the most affordable monthly premiums, Bronze and Silver tier plans are typically the way to go. Interestingly, thanks to Illinois’s new premium alignment strategy, some Gold plans may cost less than Silver ones for those who don’t qualify for Cost-Sharing Reductions (CSRs).

Here’s a closer look at Bronze and Silver plans to help you make an informed choice.

Best Bronze Tier Plans

Bronze plans are known for having the lowest monthly premiums, though they come with higher deductibles – often around $7,500 or more. These plans are ideal for generally healthy individuals who want protection against major medical expenses without a hefty monthly payment. Blue Cross Blue Shield of Illinois offers some competitive Bronze options, with an average monthly premium of about $389 for a 40-year-old.

However, it’s worth noting that Ambetter has discontinued all Bronze tier plans for 2026, which limits your options compared to previous years. If you don’t frequently require medical care, a Bronze plan could save you hundreds annually on premiums.

For those who want a bit more coverage without breaking the bank, Silver plans might be the better fit.

Best Silver Tier Plans

Silver plans strike a balance between affordable premiums and lower out-of-pocket costs. They’re also the only tier eligible for CSRs, which can significantly reduce deductibles and copays for individuals earning between 100% and 250% of the Federal Poverty Level (FPL).

"Silver plans are the sweet spot if you’re subsidy-eligible. If income is ≤ 250% Federal Poverty Level, Cost-Sharing Reductions (CSR) can shrink your deductible/copays a lot." – Nicholas Gatorano, Blank-Insurance

If you’re considering Silver plans in Illinois, Molina Healthcare and Oscar Health stand out for their competitive pricing. Molina’s Silver Saver 70 plan averages $497 per month with a $7,000 deductible, while Oscar’s Silver Classic Standard plan costs about $574 monthly with a $6,000 deductible. For those wanting a lower deductible, Cigna’s Connect Silver CMS Standard plan offers a $5,000 deductible and an $8,000 out-of-pocket maximum at approximately $610 per month.

| Carrier | Plan Name | Monthly Premium* | Deductible | Out-of-Pocket Max |

|---|---|---|---|---|

| Molina | Silver Saver 70 | $497 | $7,000 | $10,150 |

| Oscar | Silver Classic Standard | $574 | $6,000 | $8,900 |

| Cigna | Connect Silver CMS Standard | $610 | $5,000 | $8,000 |

*Premiums shown are for a 40-year-old individual without subsidies.

When choosing a plan from budget-friendly carriers like Molina or Oscar, it’s crucial to check if your preferred healthcare providers are in-network. These plans often use narrower HMO or EPO networks, which require you to stick to their approved provider lists to get coverage.

Mid-Range Plans That Balance Cost and Coverage

Mid-range health plans, sitting between Silver and Gold tiers, strike a balance by offering higher premiums in exchange for lower deductibles and out-of-pocket expenses. This setup can significantly reduce your costs when you need medical care. Interestingly, in 2026, Illinois saw a surprising pricing trend: Gold plans averaged $727 per month, while Silver plans averaged $888. This made Gold plans a more budget-friendly choice for those not eligible for subsidies.

This price reversal highlights the importance of directly comparing Silver and Gold plans. Typically, Silver plans cover about 70% of healthcare costs, while Gold plans cover 80%. However, with Gold plans offering lower premiums in 2026, they became an unexpected cost-saving option. That additional 10% in coverage often translates to lower deductibles and copays for doctor visits or prescriptions. For example, Ambetter’s Everyday Gold plan features a $750 individual deductible with a $7,000 out-of-pocket limit, while the Clear Silver plan has a much higher $7,000 deductible but the same out-of-pocket maximum. This unexpected shift in pricing encourages a closer look at how these two tiers perform in practical scenarios.

Silver and Gold Tier Plans

Let’s break down the benefits of each tier. Silver plans are especially appealing if your annual income ranges between $15,650 and $39,125 (for an individual). At this income level, you qualify for Cost-Sharing Reductions, which can lower your share of costs to as little as 6% to 27%. This makes Silver plans a strong choice for those eligible for these reductions. For example, Cigna’s Silver-4 CMS Standard plan, offered in counties like DuPage and Lake, provides a $0 deductible and no copays for primary care visits.

Gold plans, on the other hand, are ideal for people with chronic conditions or those who anticipate frequent medical care. For instance, Ambetter’s Standard Gold plan charges $25 for a primary care visit and $55 for specialist visits, compared to $50 and $100 respectively under its Standard Silver plan. Blue Cross and Blue Shield of Illinois also stands out with its 5-star rating for member experience, offering both Silver and Gold plans with the broadest provider network in the state.

"If you are in a Silver plan, it’s especially important for you shop and compare. You may find a Gold plan for a better price than your Silver plan."

– Get Covered Illinois

To determine which plan works best for you, calculate your total annual costs by combining 12 months of premiums with estimated deductibles and copays. While Gold plans may have higher premiums, their lower costs for specialists and prescriptions could make them a smarter choice for those expecting frequent care. These mid-range plans provide a solid option for people who need enhanced coverage compared to basic ACA plans.

Medicare Advantage Plans for Seniors on a Budget

If you’re a senior in Illinois looking for affordable healthcare options, Medicare Advantage plans might be worth exploring. In 2026, Illinois residents will have access to 157 Medicare Advantage plans, including at least one with a $0 premium option. The average monthly premium for these plans is $8.51.

While there are no 5-star plans available for 2026, several providers offer highly rated options, including 4.5-star and 4-star plans.

Essence Healthcare stands out with its 4.5-star HMO plans featuring $0 premiums and an average maximum out-of-pocket (MOOP) cost of $3,900. For example, their Essence Advantage Select plan includes $0 deductibles for both health and drug coverage, helping to shield you from unexpected medical expenses. Meanwhile, Cigna HealthCare offers 4-star HMO plans with $0 premiums, a low $3,000 average MOOP, enhanced Part D drug coverage, and fitness memberships. Other solid choices include Humana and Aetna, both offering 4.5-star plans with $0 premiums, giving seniors several reliable options.

"There aren’t any 5‑star plans in Illinois for 2026. But you can find 4.5‑star plans from Aetna, Essence Healthcare and Humana, and 4‑star plans from a few more companies." – Alex Rosenberg, Lead Writer, NerdWallet

These plans also come with a range of supplemental benefits that can add significant value beyond basic coverage.

Medicare Advantage plans often include perks that Original Medicare doesn’t cover. These can range from dental care with $0 copays and vision allowances (typically $100 to $500) to hearing coverage, fitness memberships like SilverSneakers, transportation services, and telehealth options. However, it’s essential to double-check that your prescriptions are included in the plan’s formulary and that your preferred doctors are in-network, especially since most HMO plans only cover out-of-network care in emergencies.

| Provider | CMS Star Rating | Monthly Premium | Avg. Out‑of‑Pocket Max | Key Benefits |

|---|---|---|---|---|

| Essence Healthcare (HMO) | 4.5 | $0 | $3,900 | Enhanced drug benefits, coordinated care |

| Cigna HealthCare (HMO) | 4.0 | $0 | $3,000 | Enhanced Part D coverage, fitness memberships |

| Humana (HMO) | 3.5 – 4.5 | $0 | $3,091 | Part B Giveback options, USAA Honor plans |

| Aetna | 4.0 – 4.5 | $0 | Varies | SilverSneakers, dental, vision, hearing |

| UnitedHealthcare | 4.0 | $0 | $4,427 | Large provider network, $0 Tier 1 & 2 drugs |

When comparing plans, pay close attention to the MOOP limit. While $0 premiums sound appealing, they can sometimes hide higher out-of-pocket costs, with some MOOPs reaching up to $9,250. Plans like Cigna’s ($3,000 MOOP) and Humana’s ($3,091 MOOP) offer better financial protection against unexpected medical bills. For instance, in Dupage County, 43 out of 54 plans have $0 premiums, with an average MOOP of $4,797. However, in Wayne County, the average MOOP jumps to $6,309. This variation highlights why it’s crucial to evaluate both the premium and MOOP when choosing a plan that fits your budget and healthcare needs.

Medicaid and Low-Income Coverage Options

Medicaid offers $0 premium coverage for eligible residents in Illinois. As of October 2025, more than 3 million people in the state relied on Medicaid or CHIP, making it a critical resource for those seeking affordable healthcare options. The program covers a wide range of services, including doctor visits, hospital stays, emergency care, prescription medications (with copays typically between $2 and $3.90), dental care, vision services, and mental health treatment.

Eligibility is based on income and household size. For low-income adults aged 19-64, the income limit is $1,835 per month for a single person or $3,795 for a family of four (138% of the Federal Poverty Level). Children can qualify under the All Kids program, which has much higher income thresholds – up to $8,745 monthly for a family of four (318% FPL). Pregnant women are eligible with income up to $3,841 for a household of two (213% FPL). Notably, Illinois was the first state to provide full Medicaid benefits to mothers for 12 months postpartum. For seniors aged 65+ or individuals with disabilities, the requirements are stricter, with income limits around $1,304 per month for individuals and an asset limit of $17,500.

How to Apply:

You can apply online, by phone, in person, or through a paper application. The easiest method is online through the Application for Benefits Eligibility (ABE) portal at abe.illinois.gov. Alternatively, you can call 1-800-843-6154. Before starting your application, gather essential documents like your Social Security number, proof of residency, and recent income records. Applications are typically processed within 45 days, although disability-related cases may take up to 60 days.

"Applying online is the best way to keep track of what information you submitted in case you need to make any changes." – Illinois Department of Healthcare and Family Services

Important Tips for Applicants:

- Watch for a Verification Checklist (VCL) in the mail. If you receive one, you must respond within 10 days to avoid having your application denied.

- Medicaid coverage can sometimes be backdated to cover medical bills from up to three months prior to your application date, which can be a significant benefit if you’ve had recent healthcare expenses.

- For seniors or individuals with disabilities who exceed income limits, Illinois offers a "spenddown" program. This works like a deductible – once you pay a set amount of medical expenses each month, Medicaid will cover the rest.

Medicaid serves as an essential safety net, offering affordable healthcare options tailored to the needs of different groups. It’s a critical resource for those navigating the complexities of healthcare coverage.

The Role of Expert Guidance in Plan Selection

Choosing the right health insurance plan involves more than just comparing premiums. You need to understand network details, formularies, and metal tiers to make an informed choice. With 11 on-exchange insurers offering diverse networks and the state’s transition to the new Get Covered Illinois platform starting November 1, 2025, the process can feel overwhelming. This is where a licensed health insurance broker can make all the difference. They simplify the selection process and often uncover hidden savings and benefits.

For example, in 2026, a family of four earning up to $128,600 may still qualify for premium tax credits. Additionally, Cost-Sharing Reductions (CSR) are available exclusively for Silver plans to households earning between 100% and 250% of the Federal Poverty Level. These reductions can significantly lower out-of-pocket costs, ranging from $1,000 to $4,000 annually.

"Licensed health insurance agents provide free enrollment assistance for Illinois marketplace plans, Medicaid, and All Kids applications. Agents are compensated by insurance carriers, not by consumers, so using an agent costs the same as enrolling directly through Get Covered Illinois." – ForHealthInsurance.com

Local expertise is critical, especially since plan availability and provider networks vary by ZIP code and county. A knowledgeable broker ensures that your preferred providers, such as Northwestern Medicine or Advocate Health Care, are in-network. They also check prescription drug formularies to confirm your medications are covered, helping you avoid unexpected expenses.

Expert guidance can also help you sidestep costly mistakes. For instance, enrolling directly with an insurance carrier outside the official marketplace means you forfeit eligibility for subsidies. Brokers calculate your total annual costs by combining premiums with expected out-of-pocket expenses, ensuring you don’t sacrifice coverage for the sake of a lower premium. They might also recommend strategies like enrolling adults in Marketplace plans while placing children in All Kids to minimize overall household costs.

Illinois Health Agents offer this personalized, local support at no extra cost, helping individuals, families, and businesses find comprehensive coverage while maximizing financial assistance. This kind of expert help ensures you’re making a well-informed decision tailored to your needs.

Conclusion

Choosing health insurance in Illinois means weighing monthly premiums against the real costs of care. For example, while a Bronze plan might have a premium of about $384 per month, it could also come with a hefty $7,000 deductible when you actually need care. To get a clearer picture of your annual costs, factor in premiums, deductibles, copays, and out-of-pocket maximums. These calculations are crucial as you prepare for upcoming changes.

Big shifts are on the horizon for Illinois health plans in 2026. That year marks the debut of Get Covered Illinois, the state’s new platform replacing the federal marketplace. Additionally, the expiration of enhanced federal tax credits could lead to significant premium increases – up to 78% on average statewide. For instance, a low-income individual might see their monthly costs jump from $0 to over $60, while higher-income couples could face premiums as high as $2,200 without subsidies.

"We’re really encouraging people, don’t walk away. Come and talk to a navigator… There might be an option that will be affordable for you."

- Ann Gillespie, Director, Illinois Department of Insurance

This advice highlights the importance of carefully comparing plans. With seven carriers offering a range of networks and benefits, it’s essential to check if your preferred doctors, hospitals, and prescriptions are covered.

As the market evolves, expert guidance becomes even more valuable. Illinois Health Agents offer personalized, local support at no additional cost. They can help you navigate these changes, maximize subsidies, and find coverage that fits your budget. With around 90% of marketplace enrollees receiving tax credits, working with an expert ensures you don’t miss out on financial assistance.

FAQs

How do I estimate my total yearly cost, not just the monthly premium?

To figure out your yearly health insurance costs, start by calculating your annual premium (multiply your monthly premium by 12). Then, add in possible out-of-pocket expenses such as deductibles, copayments, coinsurance, and the out-of-pocket maximums. For ACA plans in Illinois, the out-of-pocket maximums for 2025 are estimated at about $9,200 for individuals and $18,400 for families. Be sure to consider any subsidies or financial assistance that might reduce your overall expenses.

Should I choose Bronze, Silver, or Gold if I don’t qualify for CSRs?

If you don’t qualify for cost-sharing reductions (CSRs), Gold or Platinum plans might be a better choice since they come with lower out-of-pocket expenses. On the other hand, Bronze and Silver plans typically have lower monthly premiums but higher deductibles. When choosing, think about your healthcare needs and what fits your budget best.

What should I check first to avoid out-of-network or drug coverage surprises?

When evaluating a plan, it’s crucial to check the provider network and formulary. Confirm that your preferred doctors and medications are included. This helps you avoid surprise out-of-network charges or uncovered prescriptions, ensuring the plan aligns with your healthcare needs.

Recent Comments